This page includes sophisticated financial research and educational information that is intended only for investment professionals and other knowledgeable institutional investors who are capable of evaluating investment risks and making their own investment decisions. It should not be interpreted as investment advice or as a recommendation of any particular security, strategy or investment product.

Factor Investing

Factors are one of the building blocks of a systematic approach. They define the characteristics of attractive and unattractive stocks and provide a consistent, rules-based implementation of an investment philosophy. How does it work? In a long-only portfolio, a systematic factor strategy will overweight stocks that rank highly on a certain factor and underweight stocks that rank poorly on that factor. Using factors allows us to explain exactly why the portfolio is positioned the way it is and what the drivers of return are—every time.

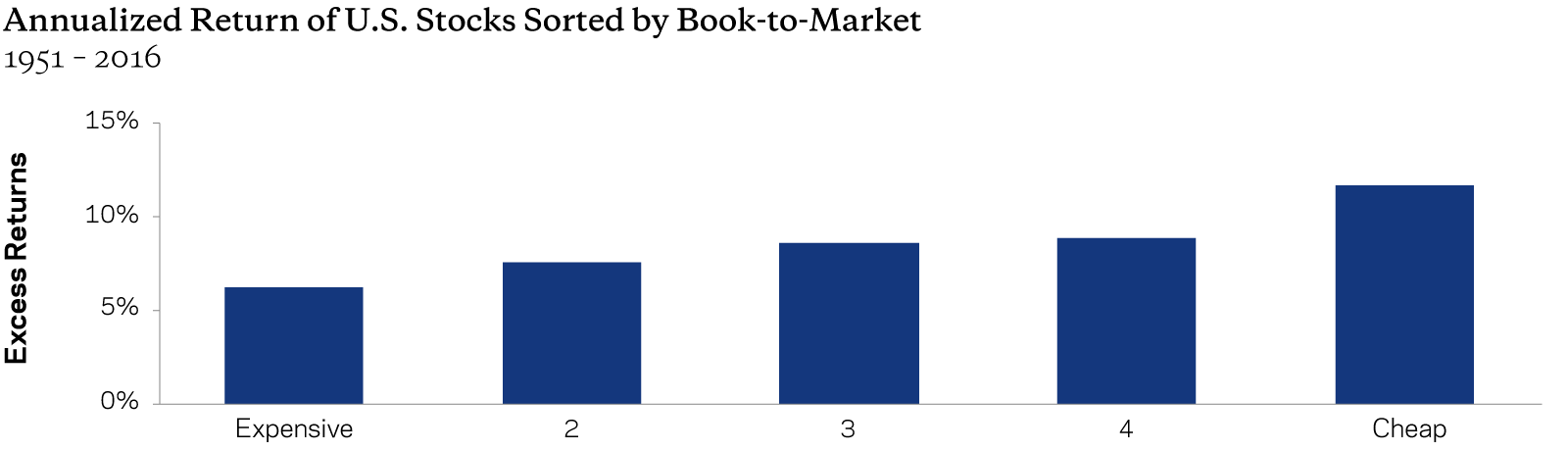

Value

Value investing is one of the best-known and most-studied approaches to outperforming the broader market over the long term. Equity valuations can be quantified by the ratio of a fundamental anchor—like book value, earnings or cash flows—over price. There are many ways to measure the valuation of a stock—we find that using a combination of measures yields the most robust results.

Sources: AQR and Kenneth R. French Data Library. Portfolios from Kenneth R. French Data Library formed based on book-to-market; quintiles are equal-weighted; returns are excess of cash. Returns sourced from “Portfolios Formed on Book-to-Market.” See Kenneth R. French Data Library for further details. These are not the returns of an actual portfolio AQR manages and are for illustrative purposes only. Past performance is not a guarantee of future performance.

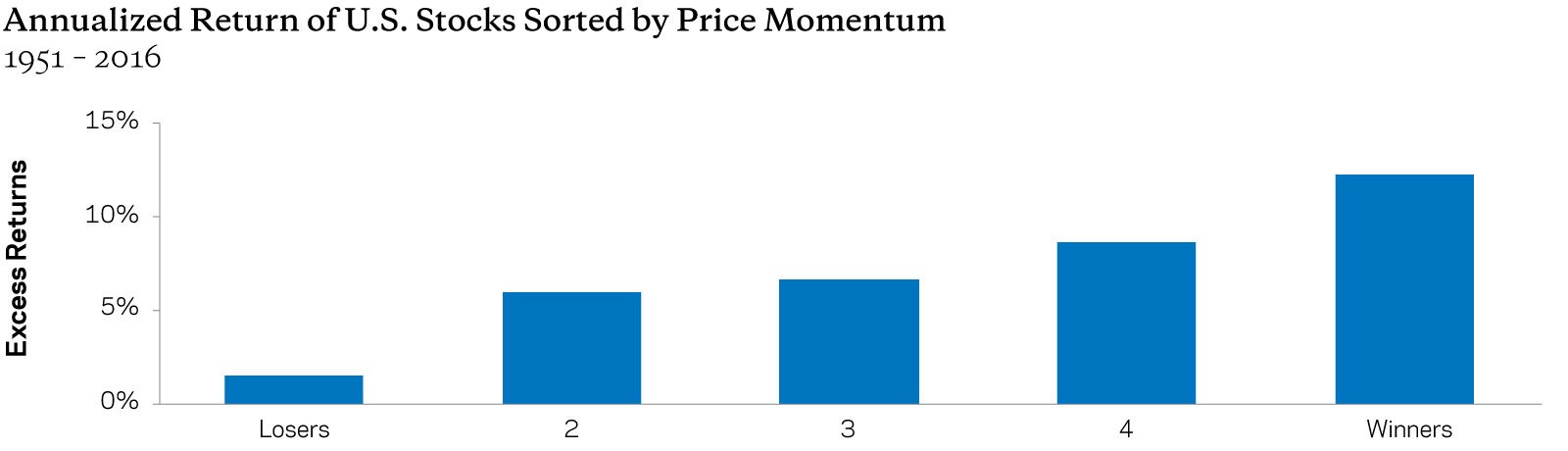

Momentum

Simply put, momentum is the idea that assets that have recently outperformed will tend to do better than assets that have recently underperformed. This tendency has been documented in at least as many asset classes as value and over even longer histories. A simple yet common measure of momentum is the last 12-months price return of an asset. Importantly, the returns of the momentum premium have tended to be negatively correlated to those of the value premium—which means they may offer investors great diversification benefits.

Source: AQR and Kenneth R. French Data Library. Portfolios from Kenneth R. French Data Library formed based on 12-month momentum, skipping most recent month; quintiles are equal-weighted; returns are excess of cash. Returns sourced from “10 Portfolios Formed on Momentum.” See Kenneth R. French Data Library for further details. These are not the returns of an actual portfolio AQR manages and are for illustrative purposes only. Past performance is not a guarantee of future performance.

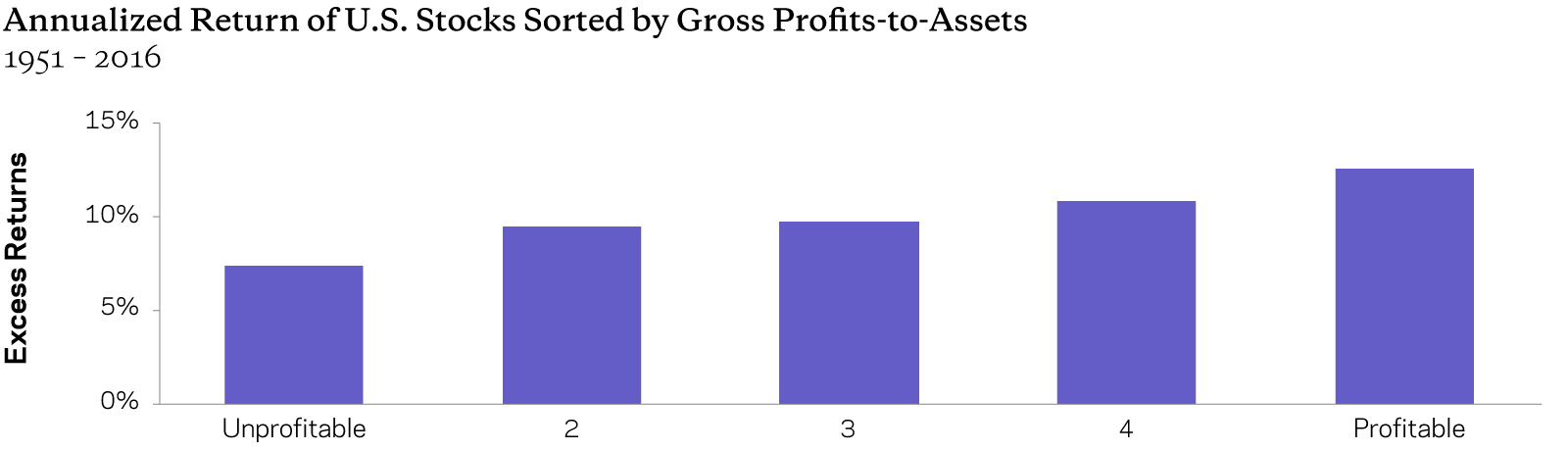

Defensive

Defensive stocks tend to be low-risk, stable or safe. As with most factors, there is more than one way to characterize a defensive company—from purely fundamental measures such as profitability and general quality to statistical measures such as low beta and low volatility. We find that both may help identify attractive stocks. For example, a defensive portfolio is likely to go long or overweight stocks that rank high on earnings quality and profitability and rank low on beta and volatility.

Source: AQR and CRSP/Compustat data. Portfolios formed based on gross profits-to-assets using all stocks in the CRSP universe; quintiles are equal-weighted; returns are excess of cash. These are not the returns of an actual portfolio AQR manages and are for illustrative purposes only. Past performance is not a guarantee of future performance.

Combining Factors into a Multi-Factor Portfolio

The combination of multiple factors has been shown to be more effective than any one individually. But how you combine them matters.

For example, how would you build a portfolio that seeks to capture both value and momentum premia? The easiest approach would be to separately buy the stocks that look most attractive from a value perspective and also buy the stocks that look most attractive from a momentum perspective. This is essentially constructing an aggregate portfolio by mixing stand-alone-style portfolios.

We believe there’s a better way. Theoretically and empirically, we find that buying stocks that look attractive from both value and momentum perspectives is more effective than considering each factor separately. In other words, applying investment themes in an integrated manner may be better than mixing individual styles in an “a la carte” manner.

Source: AQR

Factor Diversification Versus Timing

Factors may offer long-term sources of returns, but that doesn’t mean they make money at the time. Can investors do better—can factors be successfully timed?

Factors (like many other sources of return) can become cheap or expensive compared to their histories. It might seem intuitive to test the efficacy of factor timing by overweighting a factor when it’s cheap and underweighting when it’s expensive.

Theoretically and empirically, we find it’s not so easy. Factor timing, especially contrarian factor timing, is far from an efficient way to make returns. Why? First, there is only a weak predictive relationship between how cheap a factor might seem and its future returns. Second, we find the returns from contrarian factor timing are meaningfully correlated to the returns from the value factor itself. What that means for factor investors is there’s only limited benefit (if any at all) for portfolios that already have a value tilt or an allocation to the value factor.

Instead, we find that strategically diversifying across multiple factors to be more effective, not just in U.S. stocks, but in other geographies and asset classes too. Diversification across multiple factors doesn’t rule out timing entirely, but it raises the bar more than most investors might realize.

Factor timing is likely even harder than market timing.

Important Disclosures

This document has been provided to you solely for information purposes and does not constitute an offer or solicitation of an offer or any advice or recommendation to purchase any securities or other financial instruments and may not be construed as such. The factual information set forth herein has been obtained or derived from sources believed by the author and AQR Capital Management, LLC (“AQR”) to be reliable but it is not necessarily all-inclusive and is not guaranteed as to its accuracy and is not to be regarded as a representation or warranty, express or implied, as to the information’s accuracy or completeness, nor should the attached information serve as the basis of any investment decision. This document is intended exclusively for the use of the person to whom it has been delivered by AQR, and it is not to be reproduced or redistributed to any other person. The information set forth herein has been provided to you as secondary information and should not be the primary source for any investment or allocation decision. Past performance is not a guarantee of future performance.

This material is not research and should not be treated as research. This paper does not represent valuation judgments with respect to any financial instrument, issuer, security or sector that may be described or referenced herein and does not represent a formal or official view of AQR. The views expressed reflect the current views as of the date hereof and neither the author nor AQR undertakes to advise you of any changes in the views expressed herein.

The information contained herein is only as current as of the date indicated, and may be superseded by subsequent market events or for other reasons. Charts and graphs provided herein are for illustrative purposes only. The information in this presentation has been developed internally and/or obtained from sources believed to be reliable; however, neither AQR nor the author guarantees the accuracy, adequacy or completeness of such information. Nothing contained herein constitutes investment, legal, tax or other advice nor is it to be relied on in making an investment or other decision. There can be no assurance that an investment strategy will be successful. Historic market trends are not reliable indicators of actual future market behavior or future performance of any particular investment which may differ materially, and should not be relied upon as such.

The information in this paper may contain projections or other forward-looking statements regarding future events, targets, forecasts or expectations regarding the strategies described herein, and is only current as of the date indicated. There is no assurance that such events or targets will be achieved, and may be significantly different from that shown here. The information in this document, including statements concerning financial market trends, is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons.

Note to readers in Australia: AQR Capital Management, LLC, is exempt from the requirement to hold an Australian Financial Services License under the Corporations Act 2001, pursuant to ASIC Class Order 03/1100 as continued by ASIC Legislative Instrument 2016/396, ASIC Corporations (Amendment) Instrument 2021/510 and ASIC Corporations (Amendment) Instrument 2022/623. AQR is regulated by the Securities and Exchange Commission ("SEC") under United States of America laws and those laws may differ from Australian laws.

Note to readers in Canada: This material is being provided to you by AQR Capital Management, LLC, which provides investment advisory and management services in reliance on exemptions from adviser registration requirements to Canadian residents who qualify as “permitted clients” under applicable Canadian securities laws. No securities commission or similar authority in Canada has reviewed this presentation or has in any way passed upon the merits of any securities referenced in this presentation and any representation to the contrary is an offence.

Note to readers in Europe: AQR in the European Economic Area is AQR Capital Management (Germany) GmbH, a German limited liability company (Gesellschaft mit beschränkter Haftung; “GmbH”), with registered offices at Maximilianstrasse 13, 80539 Munich, authorized and regulated by the German Federal Financial Supervisory Authority (Bundesanstalt für Finanzdienstleistungsaufsicht, „BaFin“), with offices at Marie-Curie-Str. 24-28, 60439, Frankfurt am Main und Graurheindorfer Str. 108, 53117 Bonn, to provide the services of investment advice (Anlageberatung) and investment broking (Anlagevermittlung) pursuant to the German Securities Institutions Act (Wertpapierinstitutsgesetz; “WpIG”). The Complaint Handling Procedure for clients and prospective clients of AQR in the European Economic Area can be found here: https://ucits.aqr.com/Legal-and-Regulatory.

Note to readers in Hong Kong: The contents of this presentation have not been reviewed by any regulatory authority in Hong Kong .AQR Capital Management (Asia) Limited is licensed by the Securities and Futures Commission ("SFC") in the Hong Kong Special Administrative Region of the People's Republic of China ("Hong Kong") pursuant to the Securities and Futures Ordinance (Cap 571) (CE no: BHD676). Note to readers in China: This document does not constitute a public offer of any fund which AQR Capital Management, LLC (“AQR”) manages, whether by sale or subscription, in the People's Republic of China (the "PRC"). Any fund that this document may relate to is not being offered or sold directly or indirectly in the PRC to or for the benefit of, legal or natural persons of the PRC. Further, no legal or natural persons of the PRC may directly or indirectly purchase any shares/units of any AQR managed fund without obtaining all prior PRC’s governmental approvals that are required, whether statutorily or otherwise. Persons who come into possession of this document are required by the issuer and its representatives to observe these restrictions.

Note to readers in Singapore: This document does not constitute an offer of any fund which AQR Capital Management, LLC (“AQR”) manages. Any fund that this document may relate to and any fund related prospectus that this document may relate to has not been registered as a prospectus with the Monetary Authority of Singapore. Accordingly, this document and any other document or material in connection with the offer or sale, or invitation for subscription or purchase, of shares may not be circulated or distributed, nor may the shares be offered or sold, or be made the subject of an invitation for subscription or purchase, whether directly or indirectly, to persons in Singapore other than (i) to an institutional investor pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore (the “SFA”)) or (ii) otherwise pursuant to, and in accordance with the conditions of, any other applicable provision of the SFA .

Note to readers in Korea: Neither AQR Capital Management (Asia) Limited or AQR Capital Management, LLC (collectively “AQR”) is making any representation with respect to the eligibility of any recipients of this document to acquire any interest in a related AQR fund under the laws of Korea, including but without limitation the Foreign Exchange Transaction Act and Regulations thereunder. Any related AQR fund has not been registered under the Financial Investment Services and Capital Markets Act of Korea, and any related fund may not be offered, sold or delivered, or offered or sold to any person for re-offering or resale, directly or indirectly, in Korea or to any resident of Korea except pursuant to applicable laws and regulations of Korea.

Note to readers in Japan: This document does not constitute an offer of any fund which AQR Capital Management, LLC (“AQR”) manages. Any fund that this document may relate to has not been and will not be registered pursuant to Article 4, Paragraph 1 of the Financial Instruments and Exchange Law of Japan (Law no. 25 of 1948, as amended) and, accordingly, none of the fund shares nor any interest therein may be offered or sold, directly or indirectly, in Japan or to, or for the benefit, of any Japanese person or to others for re-offering or resale, directly or indirectly, in Japan or to any Japanese person except under circumstances which will result in compliance with all applicable laws, regulations and guidelines promulgated by the relevant Japanese governmental and regulatory authorities and in effect at the relevant time. For this purpose, a “Japanese person” means any person resident in Japan, including any corporation or other entity organised under the laws of Japan.

Note to readers in United Kingdom: This material is being provided to you by AQR Capital Management (Europe) LLP, a UK limited liability partnership with its office at Charles House 5-11, Regent St., London, SW1Y 4LR, which is authorised and regulated by the UK Financial Conduct Authority (“FCA”).